The LAW FIRM OF DAYREL SEWELL, PLLC is pleased to announce its latest publication, “Shrouded in Secrecy: LLCs and High-End Real Estate”, appearing on the front page of the September 2016 issue of the Brooklyn Barrister. The Brooklyn Barrister is the official publication of the Brooklyn Bar Association.

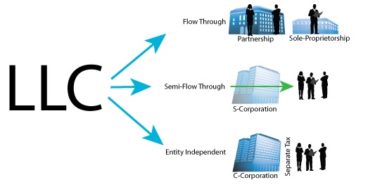

LLCs are limited liability companies that shield the owners by creating a personage that acts on behalf of the owners. This shield protects the owners from personal liability, so long as they do not create a nuisance, such as incurring large amounts of debt or causing felonies to be committed. By using LLCs as a conduit, individuals—both civilians and criminals alike—are able to purchase high-value properties while protecting their identities and similarly the funds used in the purchases.

The use of LLCs in high-end real estate transactions has increased dramatically in the last 15 years. According to an analysis for the Wall Street Journal performed by Zillow, in 2012 27% of U.S. homes sold in 2012 were bought by LLCs, as opposed to 5 years prior, when this percentage was only 17%. See Alyssa Abkowitz, Psst. Wanna Buy a House? WALL STREET JOURNAL, (Oct. 25, 2012). This growth has continued, and is particularly relevant in larger markets, such as New York.

You are encouraged to comment and receive free updates by subscribing to the firm’s Blog and Press Release sections.

Recently the Supreme Court decided the case South Dakota v. Wayfair, Inc., in which they addressed whether remote sellers of goods and services can be required to collect and remit sales taxes imposed by the consumer’s State.[1] According to S. 106, 2016 Leg. Assembly, 91st Sess. (S. D. 2016) [hereinafter “the Act”], remote sellers are required to collect and remit sales tax to the State in which the goods are sold.[2] Plaintiff, the State of South Dakota, filed of an injunction requiring respondents to register for licenses to collect and remit sales tax.[3] Respondents Wayfair, Overstock.com, Inc., and Newegg, online merchants selling goods such as furniture and electronics, moved for summary arguing that the Act is unconstitutional.[4] The Supreme Court granted certiorari to determine how to interpret precedent cases “in light of current economic realities.”[5]

Wayfair logo

In order to decide this issue, the court had to interpret and analyze the Commerce Clause and review the scope determined by two precedent cases, National Bellas Hess, Inc. v. Department of Revenue of Illinois and Quill Corporation v. North Dakota, which were decided in 1967 and 1992, respectively.[6] These cases determined that an out-of-state seller’s ability to collect and remit the tax depended on whether the seller had a physical presence in the State.[7] If the seller only permitted people to order from a catalog, it did not have a physical presence.

According to two key primary principles, state regulations cannot disfavor interstate commerce, and States cannot impose undue burdens on such commerce.[8] These principles, in combination with the

Commerce Clause, aid courts in determining outcomes in cases challenging state laws.[9] The Court laid out the guidelines for state taxation in Complete Auto Transit, Inc. v. Brady, where it held that a State can exclusively tax interstate commerce as long as the tax doesn’t create effects prohibited by the Commerce Clause. The Court determined that it would allow a tax as long as it applies to an activity with a significant connection to the taxing State, is fairly divided, doesn’t “discriminate against interstate commerce,” and is sufficiently connected to the services provided by the State.[10]

The concern about a significant connection arises from the established due process requirement that requires a business to have minimum contacts with the state in which they are selling goods or services.[11] Additionally, in Miller Brothers Co. v. Maryland, the Court held that there must be a connection between a state and the property or transaction it wishes to tax.[12]

The Court found that the physical presence rule is a flawed interpretation of the Commerce Clause in the ever-growing digital age as it gives online out-of-state businesses a significant advantage over companies with a physical presence in the state.[13] In addition, it creates market distortions.[14]

The issue of competition from online vendors has been an important one for South Dakota and the States more generally due to the fact that the States have lost revenue in the amount of $8 and $33 billion each year as a result of the rulings in Bellas Hess and Quill.[15] As a result, South Dakota residents had to “foot the bill” and pay the use tax on their purchases from other states.[16] These taxes constitute an important income source for South Dakota in funding state and local services, such as police and fire departments, as it has no state income tax.[17] Some states, such as Colorado, have imposed notice requirements on remote vendors just below collecting taxes. As a result, in the

future courts may encounter arguments regarding the meaning of physical presence.[18] Courts may also face the issue presented by small businesses seeking relief from tax collection.[19]

Consumers have moved increasingly towards online shopping in the past few years due to convenience and efficiency

Ultimately the Court overruled Quill and Bellas Hess, finding that the physical presence rule was untenable.[20] Subsequently, the Court analyzed the tax under the Complete Auto test and found that the connection between the activity and the taxing State was sufficient, as respondents had significant economic and virtual contacts with the State. However, it remains to be seen whether another Commerce Clause principle could nullify the Act.[21]

In his dissent, Chief Justice Roberts argued that Bellas Hess was incorrectly decided and that deference should be given to Congress (rather than the Courts) to determine interstate commerce issues, citing the importance of stare decisis.[22] Further, Roberts argues that the harm caused by the physical presence rule, if there is any being done, is decreasing over time.[23]

Additionally, Roberts asserts that the Court’s decision will disproportionately and arbitrarily impose unjustified costs on various goods, which will burden small businesses. He opines that imposing taxes on each sale will harm the market by increasing costs for businesses and thereby decrease the variety of goods available.[24] Roberts argues that Congress is most suited to determine competing interests of businesses and analyze the Commerce Clause and might be able to avoid such a drastic policy change and determine any retroactive effect the change might have.[25]

This ruling is vital for commercial real estate and states as stiff competition from online retailers has injured sales.[26] It will have far-reaching implications for large online venders such as Amazon, which does not currently collect state sales taxes on products of third-party sellers (in all states except Washington and Pennsylvania). Following the publication of the decision, Amazon shares tanked. Stocks of other large online marketplaces are expected to show similar decline.[27]

Amazon

As a result of the decision, South Dakota can require online out-of-state vendors that conduct sales numbering over 200 transactions or generating revenues of over $100,000 to collect taxes on items purchased by South Dakota residents. It is anticipated that other states will change their laws regarding the physical presence requirement to align similarly with South Dakota’s new requirement. It is estimated that the decision could create as much as $13 billion in tax revenue.[28] As the online market grows and improves and more stores face bankruptcy, it will be important to keep an eye out for additional legal issues and tax policies that are likely to arise in the online marketplace arena.

[1]South Dakota v. Wayfair, 138 S. Ct. 2080, 2093 (2018).

New York’s first step towards rent regulation can be traced back to the 1920s.[1] The history of rent control in New York has been a battle between owners and tenants for quite some time. In general, rent controlled apartments must be in buildings of three or more units constructed on or before February 1, 1947 and tenants must have occupied their apartment since at least July 1, 1971.[2] Under rent control, the maximum rent is determined by statute, through the Maximum Base Rent formula.[3] The Maximum Base Rent formula allows a landlord to increase monthly rent charges in order to recoup the costs of owning the building.[4] In addition, hardship increases may be allowed in specific circumstances, including when there is substantial rehabilitation to the building, and to recover the cost of major capital improvements.[5] When a rent-controlled apartment becomes vacant, it is subject to rent stabilization, or, if it does not meet the requirements of rent stabilization, it is deregulated entirely. If a rent-controlled apartment becomes vacant, and the maximum legal rent exceeds $2,000.00 instead of remaining under rent stabilization, the unit is deregulated.

Under the NYC Rent Stabilization Law, rent-stabilized apartments are subject to certain statutory rent increases, including a 20% increase for a two-year lease upon vacancy.[6] In addition, rent Stabilization Law §26-504.2 [a] provides for the deregulation of rent-stabilized apartments that reach a threshold of legal regulated rent. Specifically, deregulation will apply to:

“any housing accommodation which becomes vacant on or after [April 1, 1997] and before the effective date of the rent act of 2011 and where at the time the tenant vacated such housing accommodation the legal regulated rent was two thousand dollars or more per month; or, for any housing accommodation which is or becomes vacant on or after the effective date of the rent regulation reform act of 1997 and before the effective date of the rent act of 2011, with a legal regulated rent of two thousand dollars or more per month.”[7]

Owners have been abiding by Rent Stabilization laws for years but, when Richard Altman decided to sue his owner for illegally deregulating the unit he leased in 2003 by counting the 20% rent increase allowed by statute to push his rent over the $2,000.00 threshold, uncertainty spread throughout New York. For apartments involuntarily placed under rent regulation in New York City, those regulations were removed when a vacant apartment crossed a certain rent level. However, previously unresolved in the case law was whether, in order to effect deregulation, that rent level had to be reached during the tenancy of the last tenant prior to vacancy, or could be reached through implementation of various increases allowed to owners between two actual tenancies, such as the 20%.

Initially, in 2015 the New York Appellate Division for the First Department ruled in favor of Richard Altman, holding that although the owner was entitled to a 20% rent increase for Altman’s initial lease, that increase did not serve to deregulate the apartment because the rent was not over $2,000.00 at the time the prior tenant vacated the premises. The decision by the Appellate Division caused mass uncertainty by owners and tenants who had been previously deregulated by the 20% increase. Tenants believed they had won and were ready to start filing lawsuits to return their units to rent stabilized and collect damages for over paid rent. While tenants were excited about the court’s ruling the decision left landlords in a very difficult position because they had previously followed the law by including the 20% to deregulate the apartments and were facing potentially thousands of dollars in back-pay to tenants and thousands of apartments being re-stabilized. However, the Altman decision was appealed and heard by the New York Court of Appeals.

The Final Decision

April 26, 2018 was a monumental day for landlords who were facing potential re-stabilization of thousands of previously deregulated apartments. The Court of Appeals introduced Altman with the statement that it must determine whether the 20% vacancy increase should be included in determining if the rent of a unit exceeds the $2,000.00 threshold. To tenant’s dismay, New York’s highest Court ruled in favor of the landlords allowing vacancy rent increases to be used to boost a unit’s cost over the deregulation threshold. Ultimately, the Court of Appeals ruled that the 20% increase should be considered when determining the legal regulated rent at the time of the vacancy. The decision was a massive defeat for Altman and all other tenants hoping to re-stabilize their rent. The Court of Appeals Chief Judge Janet DiFiore wrote in her decision that state law makes it clear the vacancy rent increase should be counted when figuring if any apartment has reached the deregulation threshold. “The legislative history could not be clearer and leaves no doubt that the Legislature intended to include the vacancy increase,” DiFiore wrote.[8] The unanimous ruling by the Court of Appeals prevents the unjustified re-stablization of thousands of apartments that were appropriately deregulated according to law. It also prevents thousands of deregulated tenants from receiving a windfall in the form of a rent-stabilized apartment with a below-market rent.

New York City landscape

The New York Court of Appeals decision will continue to allow landlords to deregulate units and buildings that were once rent stabilized. In a city where rent is continuing to increase and become unaffordable, rent stabilized apartments will continue to decrease. Unfortunately, for tenants seeking rent stabilized apartments there are not many left and there will not be new rent stabilized apartments appearing on the NYC real estate horizon. The endless new construction taking place all over New York will continue to make landlords deregulate apartments and drive rent prices up. Bear in mind if you are one of the lucky few living in a rent stabilized apartment, hold on to it for as long as you can. Otherwise, it will be like looking for a need in a haystack of brand-new, highly-priced, luxury apartments.

[1] Peter D. Salins & Gerard C.S. Mildner, Scarcity By Design: The Legacy ofNew York City‘s Housing Policies, 120-21, 52-53 (1992).

The LAW FIRM OF DAYREL SEWELL, PLLC is pleased to announce that Mr. Sewell’s recent, featured publication, The Ignominious Patent Troll, also prominently appears in the year-end publication of the Brooklyn Barrister.

In Network Protection Sciences, LLC, and similar cases, courts ought to be more willing to utilize sanctions as well as the other methods discussed herein to shutter the courthouse doors to abusive litigation. It is incomprehensible to have these abusive litigation deterrents and not utilize them when the record screams otherwise. Rule 11(c) of the Federal Rules of Civil Procedure offers sanctions for litigation abuses and indicates that reasonable attorney fees can serve as one form of sanctions. Additionally, the Patent Act provides that a “court in exceptional cases may award reasonable attorney fees to the prevailing party.” See 35 U.S.C. § 285. Section 285’s language was first included in the 1946 statutory revision of damage calculations. However, rather than limiting the award to “exceptional cases”, the 1946 statute provided that “[t]he court may in its discretion award reasonable attorney’s fees to the prevailing party.” See 35 U.S.C. § 70 (1946 ed.).

It is understood that there is discretion involved in the sanction-worthy, decision-making process. Nevertheless, if rules that are available are not justly applied to appropriate situations, then there is little speculation that abusive litigation tactics will continue. As Federal Circuit Chief Judge Rader says, “[j]udges know the routine all too well, and the law gives them the authority to stop it. We urge them to do so.” See Randall R. Rader, Colleen V. Chien & David Hricik, Make Trolls Pay in Court, N.Y.TIMES, June 5, 2013, at A5.”

The Brooklyn Barrister is the official publication of the Brooklyn Bar Association. Dayrel looks forward to continuing his leadership roles as Chair of the Brooklyn Bar Association Intellectual Property Committee and Vice-Chair of the Brooklyn Bar Association Real Property Committee.

347-787-6824

347-787-6824